Abstract

In Q3 2024, there were 321 funding events, down 25.69% quarter-on-quarter, with a total of $2.406 billion raised, a 15.04% decrease. Infrastructure led with $745 million, accounting for 30.9%. Bitcoin price fluctuated widely in Q3, rising 0.8% from the quarter’s start.

Medium-scale ($5M-$10M) funding projects decreased by 30.4%, while large-scale (over $10M) projects dropped by 35.8%. Iris Energy secured the largest single funding of $413 million. Robot Ventures was the most active institution with 22 investments. The most popular project tag for active institutions (over 10 investments) was infrastructure (39.2%).

Tier1 funds are focusing on OTC as an investment theme. Solana, Bitcoin, Ton, and Base ecosystems showed leading growth. With an impending rate cut cycle lowering capital costs, Ethereum’s ecosystem continues to benefit from its DeFi leadership.

Data analysis tools, creator economy, and prediction markets emerged as new popular tags. The crypto market is favoring product-market fit (PMF). Infrastructure remains the primary choice for blockchain capital, with high concurrency potentially becoming a major narrative for public chains in the next cycle.

Projects like Monad and EigenLayer, which raised large amounts ($50M+) and gained support from top institutions/exchanges, are nearing unlock. These mainly involve L1/L2 infrastructure, LRT, and derivative DeFi. However, due to insufficient liquidity and selling pressure in H1, projects and investors are adjusting strategies, seeking cash flow and high liquidity to adapt to lower yields and stringent valuation analyses.

Q3 2024 total funding of $2.406 billion, down 15.04% QoQ; Infrastructure category funding reached $745 million

In Q3 2024, Bitcoin price showed wide fluctuations. Crypto primary market funding remained active but showed a declining trend month by month. Q3 2024 saw 321 funding rounds, down 25.69% QoQ. Total funding reached $2.406 billion, a 15.04% QoQ decrease. The average funding amount slightly increased, indicating institutions’ preference for focusing on quality projects. The median funding dropped marginally from $4.175 million to $4.15 million, suggesting that while funds decreased, institutions remained active in small to medium-scale projects. More cautious strategies also led to reduced total funding. This may be related to poor token TGE performance in H1 or market conditions mismatching early-stage project valuations and institutional investment estimates. Despite Bitcoin prices recovering to previous bull market highs in 2024, primary market funding hasn’t reached the same period’s levels. The continued decline in Q3 funding scale and number may be due to altcoin prices not rising in sync and poor token performance in H1, affecting investor confidence.

According to RootData, the top three categories by Q3 funding were Infrastructure, Others, and DeFi. Infrastructure category funding reached $745 million, accounting for 30.9% of total funding.

Notably, the “Others” category raised $453 million, 18.8% of the total. This phenomenon is driven by several factors: the continued popularity of the MeMe sector, a significant increase in AI and Crypto integration projects, and the ongoing expansion of DePin and Bitcoin ecosystems. Both investors and the market are seeking new narratives and innovations. The DeFi category ranked third with $222 million in funding, 9.2% of the total, down 31.9% QoQ. With limited market funds and attention-driven investments, DeFi projects’ lack of narrative and innovation led to a significant decrease in funding scale.

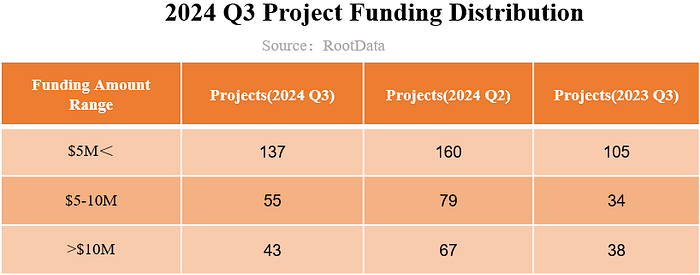

43 large-scale funding projects in Q3, up 13.2% YoY; Acquisition-type funding in Top 10 reached $681 million

Regarding funding ranges in Q3, early-stage investments (below $5M) numbered 137, down 14.4% QoQ; mid-stage investments ($5M-$10M) totaled 55, down 30.4% QoQ. Large-scale investments (above $10M) numbered 43, down 35.8% QoQ. This trend may reflect that major institutions completed their “positioning” plans in Q2, with Q3 showing a gradual slowdown in investment scale. Additionally, current difficulties in investment exits suggest a potentially significant market rise in Q4 or the near future.

The highest-funded project in Q3 2024 was Bitcoin mining company Iris Energy, raising $413 million. Following closely was Bitcoin miner Stronghold, securing $175 million through acquisition. Third was modular blockchain network Celestia, completing a $100 million OTC round at a $3.5 billion valuation. Notably, 3 of the Top 10 funded projects were acquisitions, totaling $681 million, accounting for 57.5% of the Top 10 total.

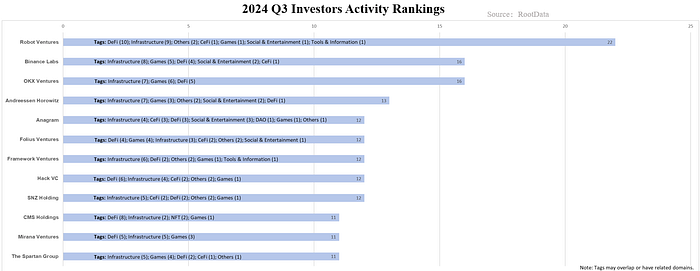

12 investment institutions made over 10 investments in Q3, with Robot Ventures being the most active, making 22 investments

According to RootData, in Q3 2024, 12 investment institutions making over 10 investments participated in a total of 160 investments. Robot Ventures led with 22 investments, focusing on projects tagged as infrastructure and DeFi. Following closely were Binance Labs and OKX Ventures, each with 16 investments. These two leading exchanges were particularly active in GamFi-tagged projects, with 5 and 6 investments respectively, showing more activity in this category compared to other institutions. Overall, infrastructure remains the most popular category, with these 12 institutions investing 65 times in projects with this tag, while DeFi-related projects received 56 investments. Additionally, DAO, NFT, and tools & information projects continued to receive less attention.

Tier1 funds are viewing OTC as an investment theme, with ecosystems like Solana, Bitcoin, Ton, and Base leading in project growth

Large single investments in Q3 occurred in the OTC market. Combining this with OTC funding from top projects like SOL, Near, and Aptos, it indicates that more Tier1 funds are viewing OTC as an investment theme. This strategy hedges against risks such as difficulties in launching new projects, liquidity tightening, and FDV (Fully Diluted Valuation) skepticism.

Contrary to market skepticism about the Ethereum ecosystem, it remains the most recognized infrastructure by investors and developers. The Ethereum ecosystem completed 67 funding rounds in Q3, totaling $481 million. With the beginning of an interest rate cut cycle, lower capital costs may drive on-chain prosperity, aiding DeFi sector recovery and innovation. Ethereum’s leadership in this sector will continue to benefit it.

According to incomplete records, ecosystems like Solana, Bitcoin, Ton, and Base are leading in project growth numbers. Ethereum still tops the public chain list with over 2,500 total applications. The crypto market is attempting to solve the “high FDV, low circulation” problem through Meme economics. Solana shines with Pump.fun, which achieved $100 million in revenue in just 217 days. Binance consecutively listed 5 Ton ecosystem projects including Catizen, Hamster Kombat, and Dogs, attracting a large influx of investors to the Ton ecosystem in a short time. The Bitcoin ecosystem may become the next user growth platform. Besides inscriptions and runes, infrastructure development is particularly rapid (e.g., Babylon, Fractal).

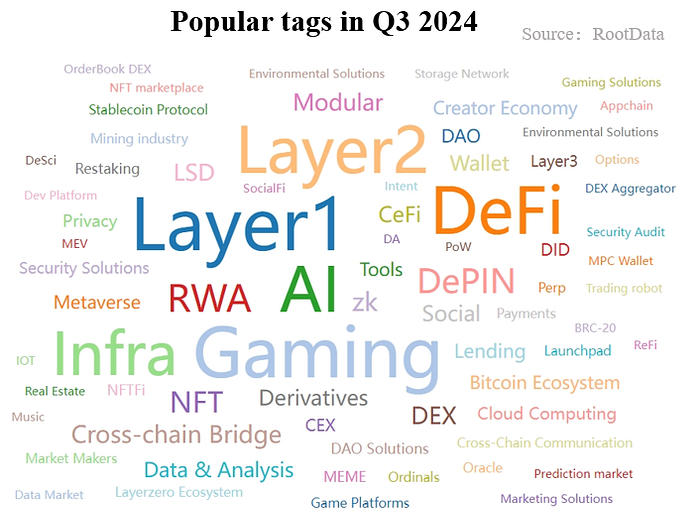

Data analysis tools, creator economy, and prediction markets emerge as new popular tags. High concurrency may become one of the main narratives for public chains in the next cycle

Based on RootData’s popular tags (over 1000 clicks), data analysis tools, creator economy, and prediction markets are rapidly gaining popularity. This could be attributed to the market influence of star projects and indicates that the crypto market is increasingly favoring products with strong product-market fit (PMF).

Data analysis tools: RootData, SoSo Value, DeFiLlama…

Creator economy: Story Protocol, Tari, Follow…

Prediction markets: Polymarket, Limitless, JogoJogo…

The infrastructure category remains the primary choice for blockchain capital, with its regulatory compliance and development prospects far superior to other types of blockchain projects. High concurrency and parallel EVM may become the next major narrative for public chains, with projects like Monad and MageETH potentially helping to achieve exponential improvements in blockchain TPS. Traditional giants continue to accelerate their layout in the Crypto industry, such as Sony launching the L2 network Soneium.

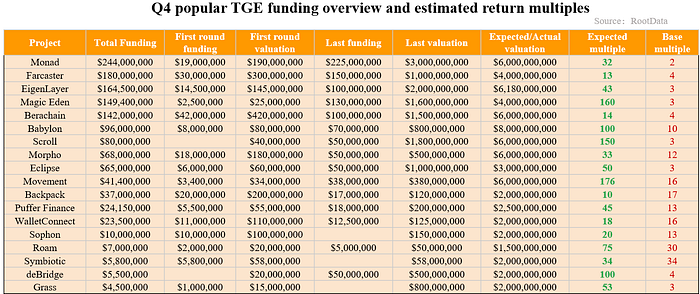

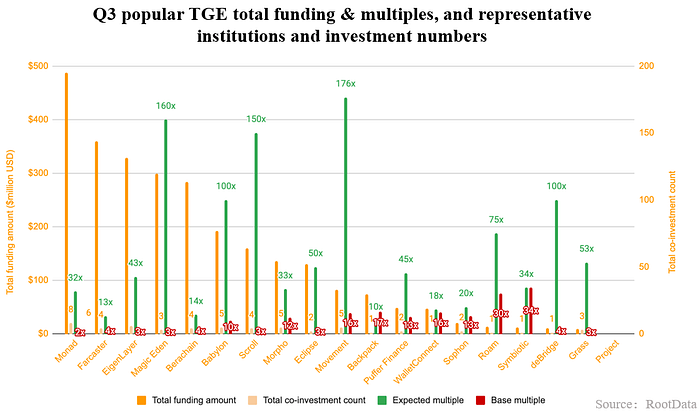

Q4 popular TGE projects revealed, Monad and other projects with tens or hundreds of millions in funding show return multiples ranging from several to hundreds of times due to different investment timings

Q4 popular TGE funding overview:

Projects with total funding exceeding $100 million include Monad, Farcaster, EigenLayer, Magic Eden, and Berachain. Projects with total funding between $50 million and $100 million include Babylon, Scroll, Morpho, and Eclipse. Projects with total funding between $10 million and $50 million include Movement, Puffer, Walletconnect, and Sophon. Projects with total funding less than $10 million include Roam, Symbiotic, deBridge, and Grass. Representative institutional investors include CEX institutions such as Coinbase, OKX, Binance, as well as leading institutions like Polychain, Hack VC, IOSG, Robot Ventures, Paradigm, Variant, a16z, and Delphi Digital.

Popular TGEs in Q4 2024 are mainly L1/L2 infrastructure, LRT and derivative DeFi, followed by Solana ecosystem, RWA and DePIN

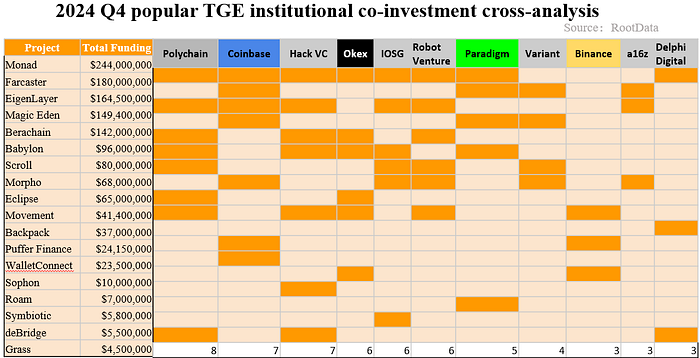

Institutional co-investments & selling pressure:

Monad received the highest funding and support from 8 top institutions, expected to list on Coinbase, Binance, and OKX, with estimated low selling pressure (32 to 2x multiple). Eigen received the third-highest funding and support from 6 top institutions, with post-TGE multiples of 43 to 3x. Unlike tokens with high multiples this year, selling pressure is moderate, and valuation may make it difficult for institutions to recover costs at first unlock. Projects with support from 4 to 5 top institutions include Farcaster, Berachain, Scroll, Babylon, Morpho, and Movement. Among these, Scroll, Babylon, and Movement are expected to have higher multiples, all backed by CEX institutions, likely achieving good exit liquidity in favorable market conditions.

Looking at Q4 popular TGE projects, L1/L2 infrastructure remains favored by the market and institutions, receiving high funding amounts and return multiples. LRT and derivative DeFi, driven by ETH AVS and interest rate research during the bear market, maintain momentum in returns and market interest from Q1 to Q4. Solana ecosystem applications, rebounding quickly after FTX’s collapse in 2021, still receive institutional and market support. RWA and DePIN, boosted by Q1 market recovery and traffic, will see institutions unlock related tokens in Q4 with considerable returns. Morpho, focusing on yield-enhancing lending, has gained support from over 5 top institutions and is worth noting.

H1 2024 TGEs faced liquidity scarcity, focus on projects with insufficient CEX co-investment to address exit channels and liquidity risks for leading projects

New narratives & exit liquidity:

Cross-analysis of popular TGE projects shows that exit channels for projects with over $10 million in funding are primarily covered by Coinbase, OKX, and Binance. Polychain, Coinbase, Hack VC, OKX, IOSG, Robot, and Paradigm welcome numerous project TGEs in Q4. The main issue facing TGEs in H1 2024 was the lack of sufficient effective exit liquidity. Investors should therefore focus on projects with large funding amounts but low CEX co-investment numbers, such as DePIN, Solana ecosystem projects, and LRT projects. In poor market conditions, these projects are expected to face selling pressure similar to H1; conversely, in liquid markets, these unlocked projects will inject liquidity into SOL and ETH ecosystems.

Q3 funding data declined overall, but institutions remained active in investing. For upcoming TGE projects, most infrastructure’s last-round institutional investors may struggle to recover costs in the first unlock due to poor altcoin performance, potentially affecting whether this liquidity enters the secondary market depending on market conditions. In contrast, Solana ecosystem, LRT, and DePIN projects still have momentum from H1. If last-round institutional investors can achieve liquidity unlocks on Binance, Coinbase, or OKX, they may recover costs in the first unlock and potentially inject liquidity into quality assets and the primary market.

Institutions should closely monitor altcoin performance to adjust niche or boutique investment strategies. Projects seeking funding should accelerate their pace, proactively lower valuations, or enhance core product competitiveness (including cash flow or industry-leading effects). Retail investors should focus on projects with higher base multiples and be aware of price volatility risks during unlocks. The industry should consider the short-term price volatility impact on risk assets due to the election results, interest rate policies, financial reports around Christmas, and liquidity outflows during the Q2 tax season next year.

Download Full Report:

EN: Crypto Investment Research Report Q3 2024

CN: Web3 行业投资研究报告 2024 Q3

VI: Báo cáo đầu tư Web3 Q3 2024

Declaration

This report is produced by RootData Research and the information or opinions expressed herein do not constitute investment strategies or recommendations for anyone. The materials, opinions, and speculations contained in this report only reflect RootData’s judgment on the day of the report’s publication, and past performance should not be used as a basis for future performance. At different times, RootData may issue reports inconsistent with the information, opinions, and speculations contained in this report. RootData does not guarantee that the information contained in this report remains up-to-date, and reliance on the information in this material is at the reader’s discretion. This material is for reference only.

About RootData

RootData is a Web3 asset discovery and tracking data platform that pioneers in encapsulating on-chain and off-chain data of Web3 assets, aiming to become a productivity tool for Web3 enthusiasts and investors with its high data structuring and readability.

Website:www.rootdata.com